Blogs

AML tips & red flags for real estate agents

AML can be a total pain - we get it. When you’re trying to onboard new customers and keep things moving, the last thing you want is to be delayed by verifying documents and endless paperwork. What it really boils down to is knowing who you’re dealing with and spotting when something doesn’t feel right. And with the right tools in place, AML can be fast, low-friction, and built into your everyday routine (rather than piling up on your desk).

For real estate agents in New Zealand, AML matters because property is one of the biggest-ticket transactions out there. It’s not about turning your agents into financial crime detectives - it’s about keeping you and your business safe from reputational damage, penalties, and, in extreme cases, criminal prosecution.

We know you already have the know-how to spot “odd” behaviour in a buyer or seller. AML is just about naming, recording and reporting it.

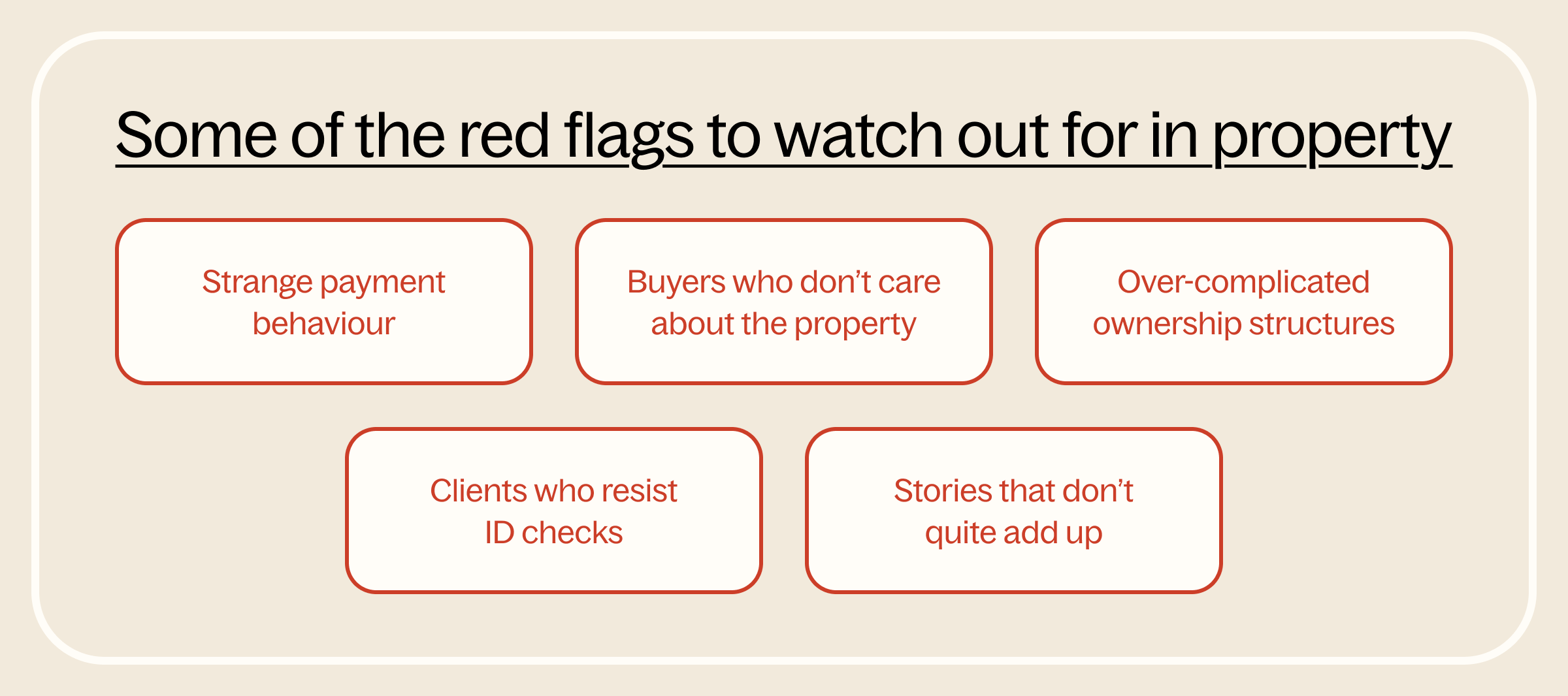

Some of the red flags to watch out for in property include:

- Strange payment behaviour

- Large cash payments or a strong push to avoid bank transfers, especially from a new client.

- A third-party payer who isn’t on the contract and has no clear link to the buyer paying deposits or settlement funds.

- Funds from high-risk places - for example, money wired from countries with weak AML controls, sanction issues, or that don’t match the buyer’s story.

- Buyers who don’t care about the property

- Minimal questions about the condition, location, or features of the home or land.

- Unusual urgency to buy quickly, even if the terms or price are not in their favour.

- Willingness to sell again soon at a loss and unconcerned about obvious downsides.

- Over-complicated ownership structures

- Layers of companies and trusts with no commercial reasoning.

- No straightforward owner.

- Reluctance to share documents and information about the companies, directors, or proof of source of funds.

- Clients who resist ID checks

- Arguing with your process or claiming the checks are unnecessary.

- Trying to use poor-quality documents or copies, with blurry photos or mismatched details.

- Avoiding face-to-face or digital biometric checks.

- Stories that don’t quite add up

- Vague explanations about occupation or income.

- Unclear sources of funds like “savings” or “investments” with no supporting documentation.

- Inconsistent details appearing across different documents

A bit of smoke might not always mean there’s a fire, but it’s important to protect yourself and your business by documenting it, asking more questions, and following your business’s AML policy.

A real estate agent doesn’t need to know every line of the legislation - they just need a simple, consistent, and repeatable way of doing vendor due diligence and risk assessment.

Top tips for real estate agents to stay AML compliant:

- Know your AML programme. There’s no point in your business having an AML programme if your agents aren’t sticking to it. Make sure all agents know what the processes are and how to stay compliant.

- Consistent ID verification for everyone, every time. Vendors and relevant parties should all have verified biometrics done for every sale. APLYiD makes this a breeze with relevant biometric AML, KYC, and KYB checks - plus, special case support is available for the less tech savvy and those without the right IDs.

- Standardise your risk questions. Ensure that you’re asking for the right information and documents consistently across all agents and branches. APLYiD’s dynamic forms can make this step a breeze.

- Create a “pause, check and escalate” rule. Ensure agents know what the red flags are, what extra steps and questions to ask when they encounter them, and who to talk to when things don’t feel right. And make sure it’s all documented.

- Report all suspicious activities to the NZ Financial Intelligence Unit and prescribed transactions of $1,000+ for international wire transfers and $10,000+ for large cash transfers.

- Keep tight records for at least 5 years after the completion of that transaction. Your AML records should be stored safely and securely. APLYiD does this automatically so that when auditors come knocking, you can quickly prove you’re meeting your AML requirements.

Without the right tech in place, this can seem like a lot of extra work for your agents. But with APLYiD, meeting your AML obligations is fast and pain free. We also keep on top of changing regulation so you can trust our platform to keep your business and processes up to scratch.

If you want simple, compliant AML without the headaches, you can book a demo and see the benefits for yourself:

- No unnecessary complexity. Just one platform for all AML tasks.

- No admin overload. ID verification, CDD, risk assessments and record-keeping - all sorted.

- No gaps in compliance. Our platform keeps you covered, even when regulations change.

- No training needed. Everything’s automated and guided.

Whether you're running a solo practice or managing a small team, APLYiD helps take the guesswork out of compliance so you can focus on what you do best.